Nov 26 (Reuters) - Fresh COVID-19 fears fuelled by a new variant rip through markets as we head towards year-end. Data points could provide the spark that re-ignites bond market ructions and a blowout U.S. jobs print and above-forecast European inflation may offer fodder to those arguing central banks need to hurry up with unwinding stimulus.

Here's your week ahead in markets from Tom Westbrook in Singapore; Dhara Ranasinghe, Karin Strohecker and Ahmad Ghaddar in London; Ira Iosebashvili and Lewis Krauskopf in New York. Compiled by Sujata Rao

1/DOVES, HAWKS & COVID

Register now for FREE unlimited access to reuters.com

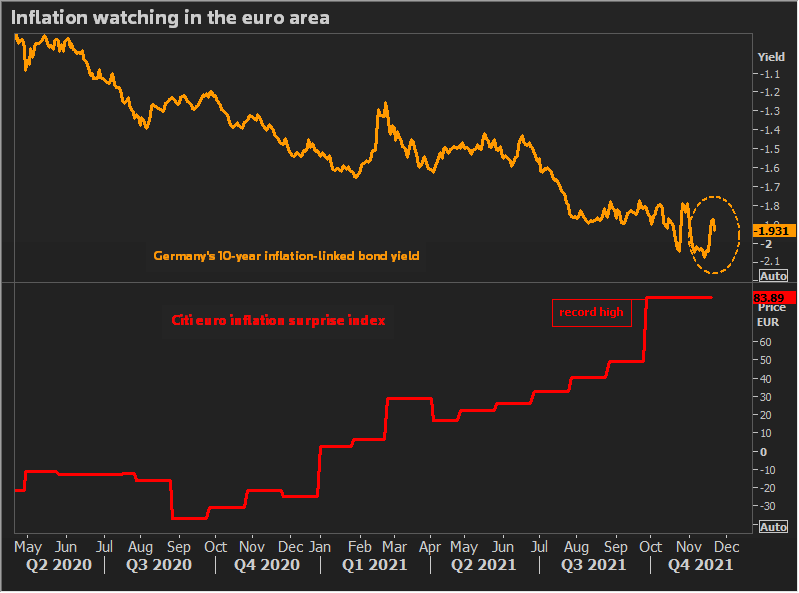

COVID-19 fears and inflation data are looming large over policy makers who have to decide the fate of two ECB bond-buying schemes in just three weeks.

Tuesday brings November flash euro zone inflation. October's print was 4.1% and many see it staying above the ECB's 2% target next year. German, Spanish and French CPI data are out Monday and Tuesday.

As inflation surges, ECB hawks warn against keeping monetary policy too loose for too long. A new German government meanwhile could raise the minimum wage by around 25%.

Their message has resonated with edgy markets. But resurgent COVID strengthens the ECB doves as Europe battles a fresh surge and news of new virus variant spreading across South Africa triggers alarm.

Renewed economic uncertainty means investors are again scaling back rate-hike bets for the U.S., euro area and Britain. The doves, it appears, have fresh ammunition to push back against those clamouring for an early end to stimulus.

2/JOBS FOR ALL

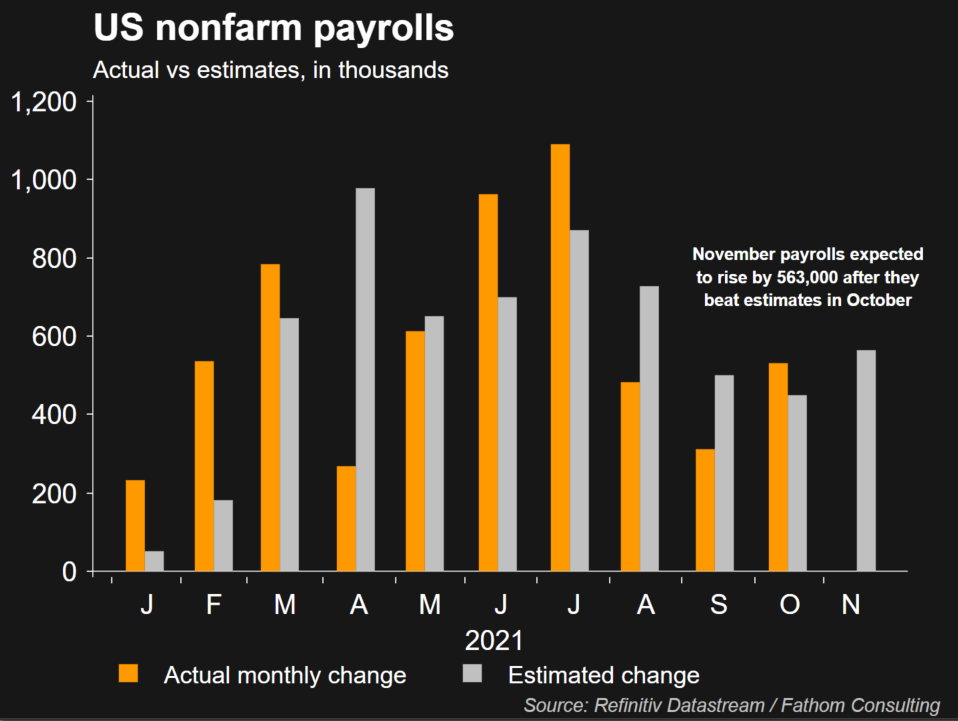

With the Federal Reserve's taper underway, a strong November employment report could bolster the case for those arguing its $120 billion-a-month bond-buying should be unwound faster.

While the Fed projects the unwinding to be complete in mid-2022, robust economic growth and inflation running at more than twice the 2% flexible average goal have sparked bets on a faster unwind and earlier rate rises.

Payroll expectations were boosted by weekly data showing jobless benefits claims at the lowest since 1969. Employers are forecast to have added 563,000 jobs, and any figure more than that could revive recent bond market ructions and mean another leg higher for the dollar.

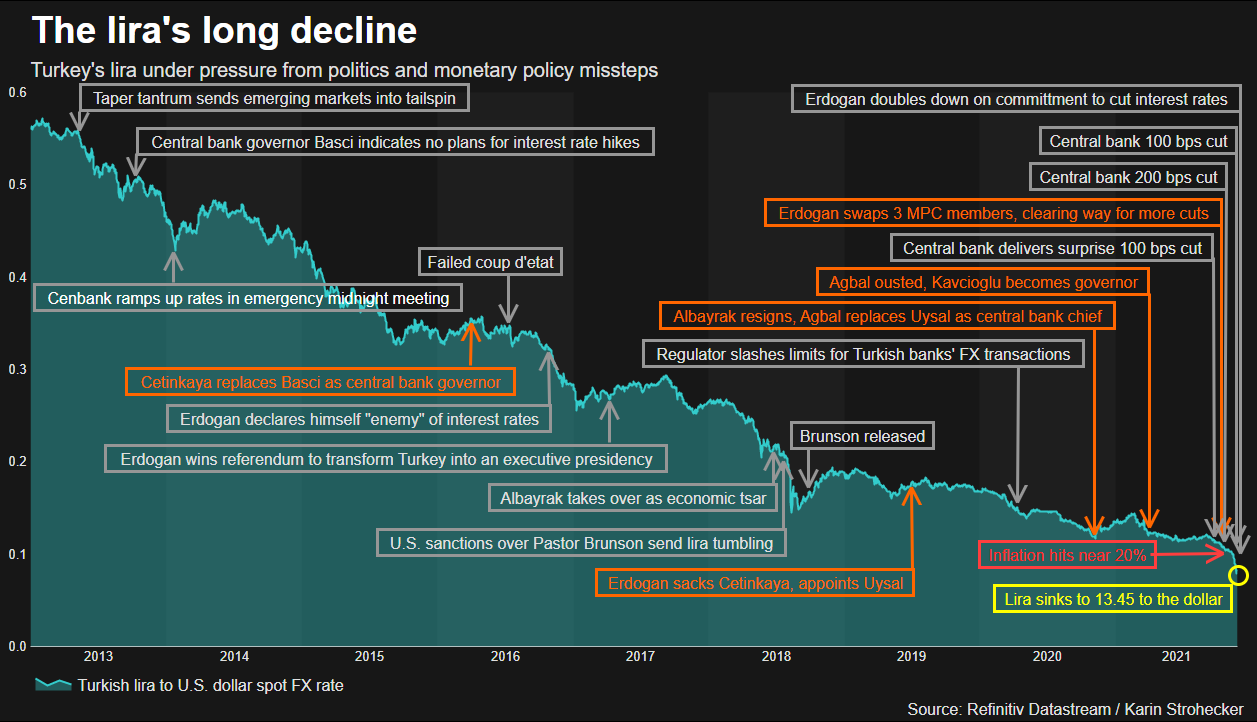

3/ TURKEY TANTRUM

Turkey just served up (another) reminder that prudent monetary policy matters - all the more so in emerging markets during times of high inflation.

President Tayyip Erdogan has doubled down on his view that double-digit inflation can be tamed by cutting interest rates. The lira has responded with a 15% plunge on Tuesday that's left it in unchartered waters.

The currency has partly recovered but the central bank may deliver another rate cut at its Dec. 16 meeting.

Monetary policy worries are stirring in Mexico, too. The peso has taken a hit after the president unexpectedly ditched his nominee for central bank governor, instead nominating a deputy finance minister.

A strengthening dollar, rising inflation and a Fed in taper mode leaves emerging market central banks precious little room for error.

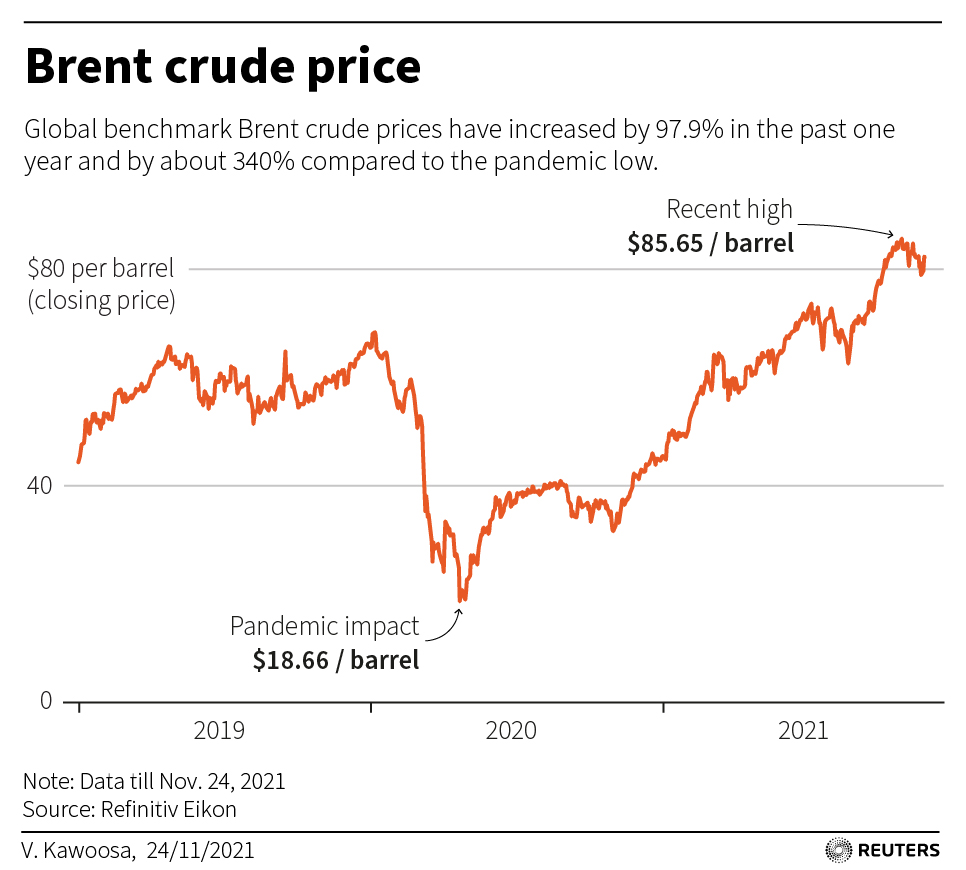

4/MORE OIL OR LESS

The OPEC+ oil producers' group has stuck to monthly output increases of 400,000 barrels per day (bpd) since August, defying consumer nations' pleas for more oil to cool $80-plus prices. Its Dec. 1-2 meeting will come just after the U.S. decision to release 50 million barrels of oil from strategic reserves.

The prospect of extra oil hasn't fazed oil markets; Goldman Sachs called it a "a drop in the ocean". Yet an OPEC+ source said the oil release by the United States and several other countries, while smaller than anticipated, would complicate its calculations.

OPEC+ production cuts will amount to 3.8 million bpd by end-December, about 4% of global consumption. Sources say there are no discussions yet about responding to the U.S. move by pausing output increases. But the group has warned the move could cause an oil glut next year.

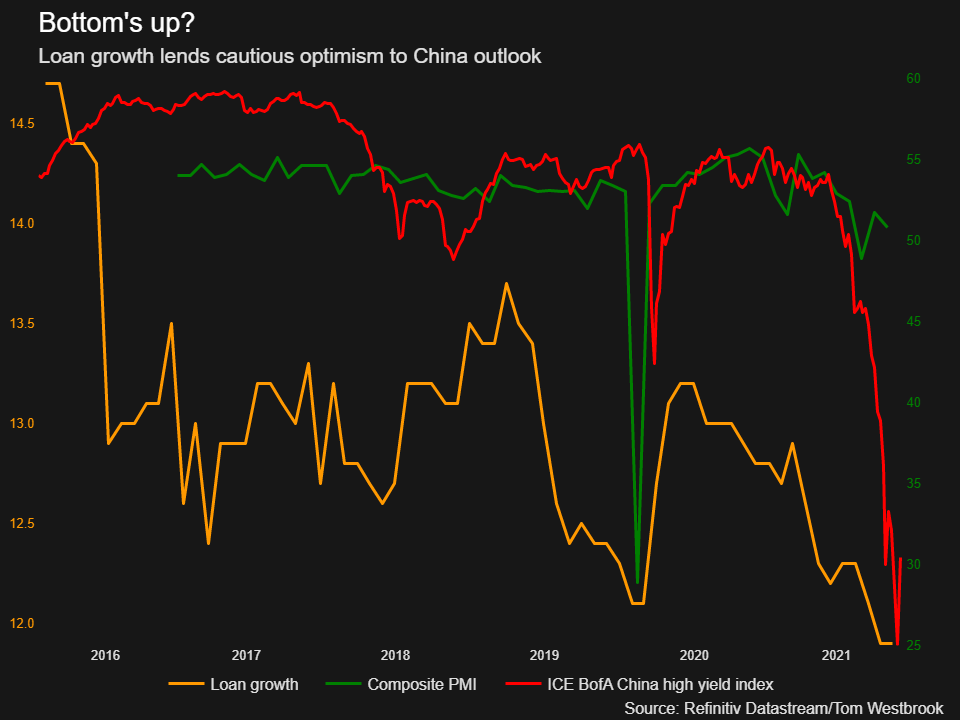

5/SLOW BUT STEADYING?

New mortgage growth is underpinning hopes the trough might be in for Chinese credit, and that the economic drag from a feared real estate calamity is starting to fade.

There are signs of a drift toward policy easing. While benchmark rates have not changed, banks are being prodded to lend to developers, authorities are seeking to cut funding costs for small business and have moved to buttress yuan stability.

Tuesday's Purchasing Managers' Indexes could show if the tide is indeed turning. But keep an eye on Dalian, where COVID is on the rise

(1 euro = 14.0991 liras)

Register now for FREE unlimited access to reuters.com

Editing by Kim Coghill

Our Standards: The Thomson Reuters Trust Principles.

"five" - Google News

November 26, 2021 at 04:32PM

https://ift.tt/3cSkYNk

Take Five: First test of December - Reuters

"five" - Google News

https://ift.tt/2YnPDf8

https://ift.tt/2SxXq6o

No comments:

Post a Comment